- Duration

3 years

- Apprentices remuneration - characteristics

Type: allowance paid by employer; fixed amount per month

Remuneration setting: centrally; as share of the national minimum wage (in the first term of the grade, see also 'Apprentices remuneration - amount'

Coverage: on- and off-the-job training

Variation(s): by the year of apprenticeship, the share of practical training within the training programme and the student's diligence and performance.- Apprentices remuneration - amount

Average regulated remuneration: EUR 61,73 (average in the first term of grade. calculation: =15% x EUR 411,52, i.e. min wage in 2017, S1)

Level in PPS per month (average): 102.71; per year (average): 1,232.51

Level in PPS per hour (average): 1.99

Share of national minimum wage (average): 15% in the first term of the first grade (Apprentices receive 10.5-19.5% of the minimum wage in the first term of the first grade depending on the share of the practical training within the training programme. Then, training provider sets the rate of mandatory increase in every term, depending on students diligence and performance)Remuneration (annual gross income) in 3 selected occupations (EUR):

hairdresser: 1st year: 773.66; 2nd: 888.67; 3rd: nap; 4th: nap

motor mechanic: 1st year: 644.72; 2nd: 740.56; 3rd: nap; 4th: nap

bricklayer: 1st year: 773.66; 2nd: 888.67; 3rd: 961.85; 4th: nap

(Exchange rate: 1 EUR = 309,90 HUF)- Time foreseen for on-the job-training

More than 50% of the overall duration of apprenticeship

Number of hours per year (average): 620

The estimate is based on the number of hours in the 3 selected occupations: hairdresser: 1st year: 916; 2nd: 651; car mechanic: 1st year: 664; 2nd: 434; bricklayer: 1st year: 500; 2nd: 626; 3rd: 465.

The number of hours depends on the qualification and the proportion of practical training. This is regulated by the framework curricula.Level: 22% (social tax) + 10% (pension) + 7% (health) of the annual gross income of apprentice

Paid by: employer (social tax) and apprentice (pension, health)

Rights: Healthcare, pension, unemployment benefit (maximum 90 days), annual leave (basically 20 working day per year), sick-leave, paid maternity leave (24 weeks)- Financing on-the-job training

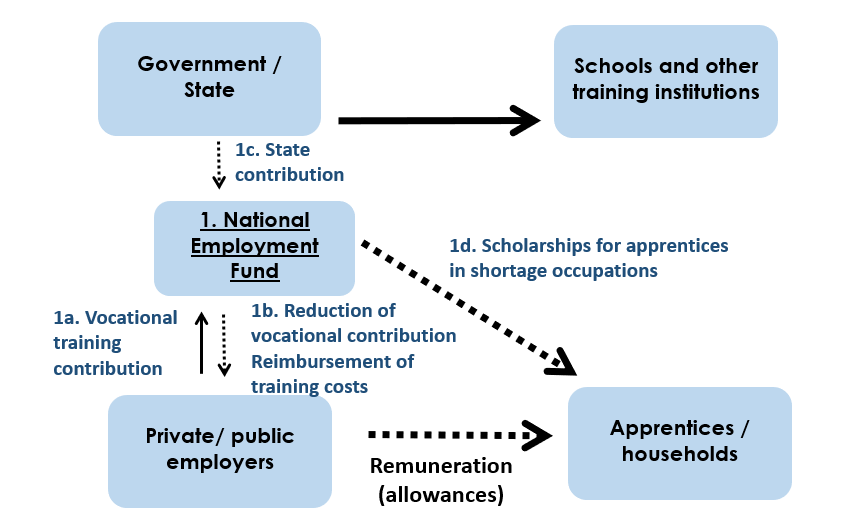

All companies pay the levy called vocational training contribution. Companies contribution obligation may be met by payment to the development and training sub-fund of the National Employment Fund or by organising practical training. In case of the latter, the contribution may be reduced based on the basic norms specified in the budget act of the given year (EUR 1,461.76/person/year in 2017).

Apprenticeship on-the-job training costs are covered by employers, including paying the allowance to the apprentices. Companies can, however, deduct the training costs from their mandatory vocational training contribution and can also have other apprenticeship-related costs reimbursed from the training sub-fund of the National Employment Fund.

In 2015, a comparative analysis of the vocational practical training basic normative amount/vocational training contribution reduction and the actual costs of practical training provided by enterprises based on apprenticeship training contract was carried out by the National Office of Vocational Education and Training and Adult Learning. This research has confirmed that the normative funding/vocational training contribution tax reduction of practical training covered most of the actual costs of practical training.

(Research can be found in the Hungarian language on the website of National Office of Vocational Education and Training and Adult Learning: http://site.nive.hu/refernet/index.php/en/publications). Based on another survey (made by the Hungarian Chamber of Commerce and Industry, Institute for Economic and Enterprise Research), according to companies' estimates vocational practical training basic normative amount/vocational training contribution reduction covers at least 80% of all training costs related to on-the-job training. The remaining cost will be covered by the enterprise.

Survey can be found in Hungarian language on the website of the Hungarian Chamber of Commerce and Industry, Institute for Economic and Enterprise Research http://gvi.hu/files/researches/486/szakiskola_2016_vallalatok_tanulmany…

- Illustration: sources of funding and financial flows

-

- Assessment of financing arrangements

Strength:

The instruments promote wide involvement of companies (employers) in VET thus giving apprentices the opportunity to acquire professional skills and competencies in a real working environment.Weaknesses:

- Only 1,3% of all companies provide apprenticeship training for VET students. It is not easy to involve companies into the VET. In Hungary 99% of all enterprises are micro, small and medium size enterprises and 95% of enterprises employ less than 10 workers.

- Only 23,6% of all VET students can take part in apprenticeship training.

- For the time being, companies do not regard the apprenticeship training as long-term investment.

- The wages provided to the apprentices are determined in tandem with the statutory minimum wage, but the support provided to the employers does not follow the annual changes of the statutory minimum wage.- Labour market outcomes

According to the results of the annual surveys, apprenticeship training increases graduates' chances of subsequent employment and of working in the vocation they trained for. The most important benefit of apprenticeship training for students is that students can socialize in a real life working environment during their apprenticeship years, their obtain skills that are high in demand and more former apprentices find a job in their qualification more easily.

- Contextual information

Statutory minimum wage: EUR 350.09 (2016, S2); EUR 411,52 (2017, S1); EUR 412,66 (2017, S2)

Average yearly working time (hours) for a full time job: 1,856

On this page: