- Duration

1-3 years (depending on the qualification level)

- Apprentices remuneration - characteristics

Type: wage paid by employer; fixed amount per month

Remuneration setting: as a share of the minimum wage. Monthly net wages are published by the Ministry of Labour. In each sector, trade unions and employers can negotiate higher percentages of the minimum wage.

Coverage: on-the-job training

Variation(s): by apprenticeship year, age of the apprentice, type of diploma- Apprentices remuneration - amount

Average regulated remuneration: EUR 725.33

This is the regulated amount for a 2nd year 18-20 year-old apprentice. This amount also equals the average wage for all 2nd year apprentices (for all age groups). Calculation: 49% x EUR 1,480.27 (i.e. the min wage in 2017)

Level in PPS per month (average): 671.6; per year (average):

Level in PPS per hour (average): not available

Share of the minimum wage: on average, 51.3% of the gross minimum wage (the share varies from 25% to 78% depending on apprentice's age and year of apprenticeship, see below).Remuneration for age groups, average annual gross income:

15-17: 1st year: 25% of the gross min wage = EUR 370.07; 2nd year: 37% of the gross min wage = EUR 547.70, 3rd year: 53% of the gross min wage = EUR 784.54

18-20: 1st year: 41% of the gross min wage = EUR 606.91; 2nd year: 49% of the gross min wage = EUR 725.33; 3rd year 65% = EUR 962.17

21 and above: 1st year: 53% of the gross min wage = EUr 784.54; 2nd year: 61% of the gross min wage = EUR 902.96 EUR; 3rd year: 78% of the gross min wage = EUR 1,154.61Remuneration (annual gross income) in 3 selected occupations (EUR):

hairdresser: 1st year: na; 2nd: na; 3rd: na; 4th: nap

motor mechanic: 1st year: na; 2nd: na; 3rd: na; 4th: nap

bricklayer: 1st year: 820; 2nd: 820; 3rd: 820; 4th: nap- Time foreseen for on-the job-training

Between 20-50% of the overall duration of apprenticeship

The number of hours varies across levels and diplomas. The law stipulates the following:

- Younger than 18 years: 8 hours a day or 35 hours a week at most. The apprentice may not work overtime.

- 18 years old and older: 10 hours a day or 35 hours a week at most. The apprentice may work overtime at most 48 hours over a week or 44 hours in average over two weeks.

Working time may vary across sectors according to the sectoral collective agreement such as hotel and restaurant industry in which working time is 39 hours a week at most.

Each training center decides for each diploma on the number of hours spent in a company. It could be 2 days at the training center and 3 days in a company, or 1 month at the training center and 1 month in a company.Paid by: the State (employers are excluded from social insurance taxes in relation to apprentices wages)

Rights: health, pension, unemployment, annual leave- Additional support for apprentice

Allowances (see 'Direct aid to apprentices') come from Regional councils to the centres for apprenticeship training, and then to apprentices.

- Financing on-the-job training

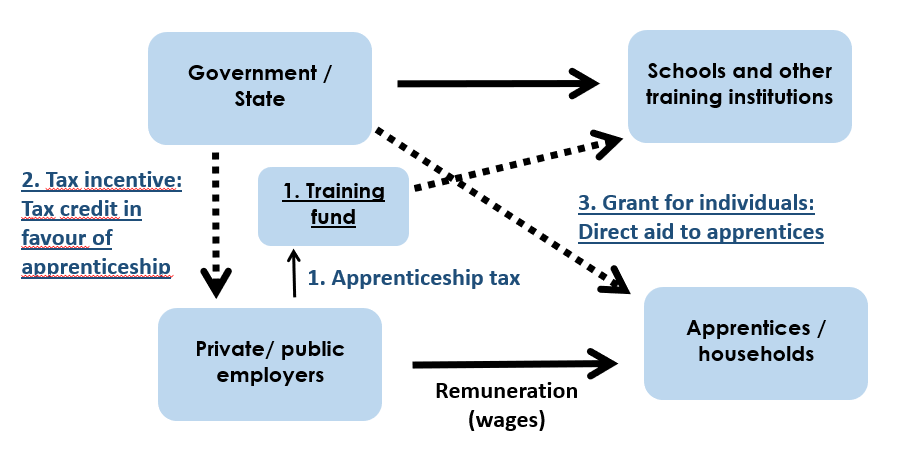

On-the-job training costs, including the apprentices' wages, are covered by employers. The State subsidises the companies through tax incentives: 'tax credit in favour of apprenticeship' and social tax exemption. In relation to the latter, the State's loss of the income revenue amounted to 1,100,000,000 in 2014.

- Financing off-the-job training

Public funding: 1,570,000,000 (2014)

Source: Cnefop; the estimation comes from publication of financing from contributors to CFA (center for apprenticeship training). It excludes the funds collected from companies through the apprenticeship training tax (to support off-the-job training), contributions from activity sectors and contributions from families/household or sales/supply of products or services.

The funds collected through the apprenticeship tax: EUR 949,000,000 in 2014.

The contributions from activity sectors: EUR 191,000,000- Illustration: sources of funding and financial flows

-

- Assessment of financing arrangements

Apprenticeship in France is largely supported by the apprenticeship tax, which is paid by all the companies that have at least one employee. The apprenticeship tax is obligatory and this can be considered as a strength. The main weaknesses are:

- Complexity and lack of transparency. Companies pay the apprenticeship to joint collecting bodies (named OCTA); but joint colleting bodies are numerous (145). The fund collection process is quite scattered. This implies regional regulation since apprenticeship lies at regional level.

- Allocation of funding may be unequal regarding type of training (low level vs. high level of apprenticeship). A part of the apprenticeship tax is allocated to training centres by the companies themselves. This lack of regulation generates inequalities, generally for the benefit of training centres delivering higher education degrees.

- A significant part of the apprenticeship tax does not support apprenticeship training. In 2010, 38% of the apprenticeship tax was allocated to technological or professional training outside apprenticeship.

Several French governments have attempted to reform the apprenticeship tax financing system to solve the complexity and lack of transparency issues. Despite the efforts to solve these issues, the apprenticeship tax financing system is considered inefficient and unequal.- Contextual information

Statutory minimum wage: EUR 1,466.62 (2016, S2); 1,480.27 (2017, S1 and S2)

Average yearly working time (hours) for a full time job: 1,616.20

On this page: